使用期限租赁或*

许可形式单机和网络版

原产地美国

介质下载

适用平台window,mac,linux

科学软件网销售软件达19年,有丰富的销售经验以及客户资源,提供的产品涵盖各个学科,包括经管,仿真,地球地理,生物化学,工程科学,排版及网络管理等。此外,我们还提供很多附加服务,如:现场培训、课程、解决方案、咨询服务等。

以上两场讲座均免费,欢迎大家报名参加。

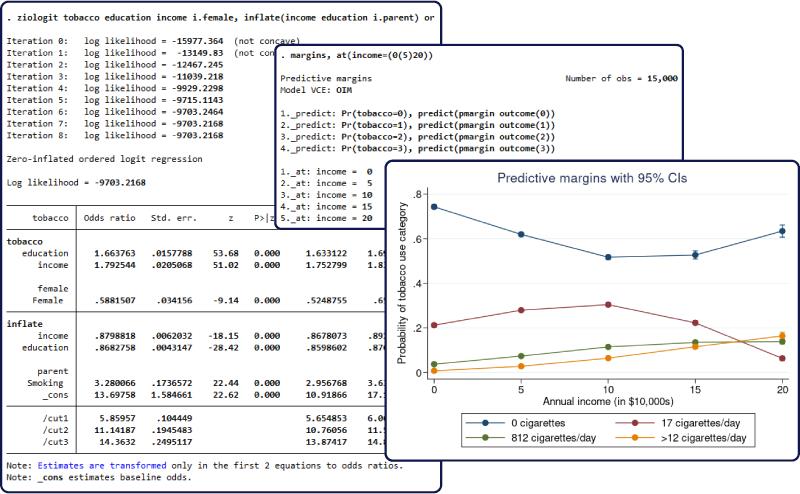

Stata 16 于2019年6月26日**发布,更新了大量的新功能,详细信息请登陆科学软件网查看。

Frequentist inference is based on the sampling distributions of estimators of parameters and provides

parameter point estimates and their standard errors as well as confidence intervals. The exact sampling

distributions are rarely known and are often approximated by a large-sample normal distribution.

Bayesian inference is based on the posterior distribution of the parameters and provides summaries of

this distribution including posterior means and their MCMC standard errors (MCSE) as well as credible

intervals. Although exact posterior distributions are known only in a number of cases, general posterior

distributions can be estimated via, for example, Markov chain Monte Carlo (MCMC) sampling without

any large-sample approximation.

Frequentist confidence intervals do not have straightforward probabilistic interpretations as do

Bayesian credible intervals. For example, the interpretation of a 95% confidence interval is that if

we repeat the same experiment many times and compute confidence intervals for each experiment,

then 95% of those intervals will contain the true value of the parameter. For any given confidence

interval, the probability that the true value is in that interval is either zero or one, and we do not

know which. We may only infer that any given confidence interval provides a plausible range for the

true value of the parameter. A 95% Bayesian credible interval, on the other hand, provides a range

for a parameter such that the probability that the parameter lies in that range is 95%.

Nonlinear DSGE models in Stata 15

In Stata 15, we introduced the dsge command for fitting linear DSGE models, which are time-series models used in economics and finance. These models are an alternative to traditional forecasting models. Both attempt to explain aggregate economic phenomena, but DSGE models do this on the basis of models derived from microeconomic theory.

New in Stata 16, the dsgenl command fits nonlinear DSGE models. Most DSGE models are nonlinear, and this means that you no longer need to linearize them by hand. When you enter equations into dsgenl, it linearizes them for you.

After estimating the parameters of your model with dsgenl, you can obtain the transition and policy matrices; determine the model’s steady state; estimate variables’ variances, covariances, and autocovariances implied by the system of equations; and create and graph impulse–response functions.

This is likely to be the favorite feature of macroeconomists and anyone working in a central bank.

2020年,北京天演融智软件有限公司申请高等教育司产学合作协同育人项目,“大数据”和“机器学习”师资培训项目,以及基于OBE的教考分离改革与教学评测项目已获得批准。我们将会跟更多的高校合作,产学融合协同育人。

http://turntech8843.b2b168.com